Overview of the latest economic events in the Czech Republic

The Czech Republic plans to increase oil imports from Italy via the upgraded TAL pipeline from April. The move follows the suspension of Russian oil imports via the Druzhba pipeline in March, which was the result of payment problems linked to sanctions against Russia.

The Ministry of Defence of the Czech Republic is seeking to raise an additional eight billion crowns to meet its commitment to spend 2 % of GDP on defence. This move is in line with international commitments and strengthens the country's defence capability.

Analysts expect the Czech National Bank (CNB) Bank Board to temporarily halt the trend of interest rate cuts. This decision reflects current economic conditions and efforts to stabilise the financial market.

The future of the Czech steel industry is uncertain. The sector faces challenges related to rising costs and competition in the European market, which may lead to a decline in production and employment in the sector.

Demand for batteries is expected to triple in the next five years. This trend indicates the growing importance of energy storage and renewable energy sources in the Czech economy.

Foreign investments and acquisitions

Prime Minister Petr Fiala said that the Czech initiative to supply ammunition to Ukraine could reach the 2024 delivery volume in 2025. Last year, the initiative, funded by several NATO allies, provided Ukraine with 1.5 million artillery shells, including 500,000 155mm rounds.

Significant events outside the Czech Republic with global impact

Swiss cement company Holcim has announced its NextGen Growth 2030 strategy, which aims to achieve 6% to 10% of annual operating profit growth by 2030 through mergers and acquisitions. Following the planned spin-off and listing of its North American division Amrize later this year, Holcim intends to become a leading partner in sustainable construction. The Amrize spin-off, with a target value of $30 billion, will be one of the largest in the industry.

Despite expectations of a recovery in US investment activity following President Trump's re-election, first quarter results were disappointing, with global investment banking fees falling by 10 % to $20.6bn. The US saw a decline of 7 % to $10.6bn, while Europe faced a 22% drop to $4.6bn. Still, European traders remain optimistic as volatility in the U.S. is starting to benefit Europe. European countries are advancing infrastructure initiatives and increasing defense spending, leading to cautious optimism about M&A activity.

The U.S. high quality corporate bond market is facing its lowest supply in five years due to economic uncertainty caused by President Trump's trade policies, particularly threats of tariffs. Expected deregulation and tax cuts were expected to boost activity, with $250-300 billion in investment-grade bonds forecast for 2025, compared to $179 billion in 2024. However, uncertainty has stalled mergers, resulting in just $8 billion ready to fund acquisitions, compared to $100 billion a year earlier. Overall, investment grade bond issuance is expected to average $1.65 trillion in 2025. Reduced supply and high investor demand could further narrow credit spreads, despite the economic slowdown.

China's President Xi Jinping has met with global CEOs, including prominent figures such as the heads of AstraZeneca, Standard Chartered and Toyota, to push the fight against protectionism and strengthen the stability of global industrial and supply chains.

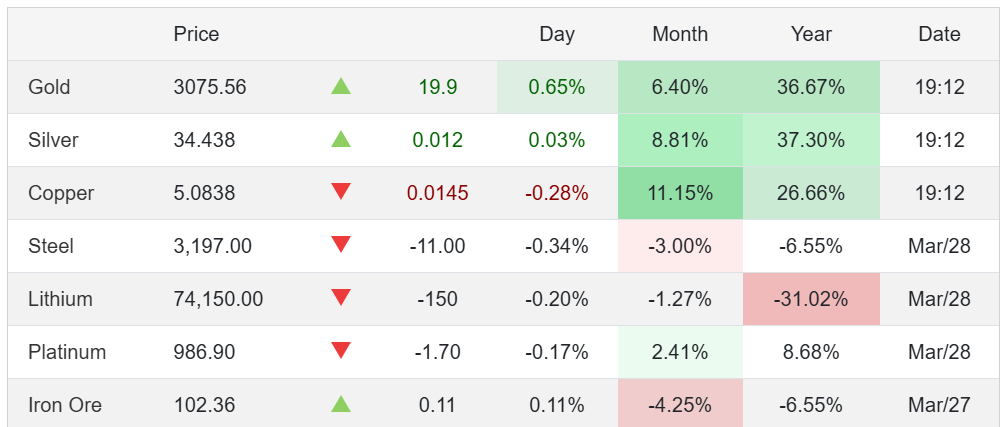

Source about precious metals and Bitcoin: tradingeconomics.com

gnews.cz - GH

Comments

Sign in · Sign up

Sign in or sign up to comment.

…