Overview of the latest economic events in the Czech Republic

Monday 30 March 2026 brings a look at the Czech economic scene ahead of a week that will be defined primarily by geopolitical tensions in the Middle East, the wait for key macro data and the fading effects of the Iranian conflict on domestic markets and consumers.

According to analysts, the turn of the first and second quarter will be marked mainly by the war in the Middle East, whose conflict has moved into the fifth week. In the Czech Republic, this week sees the release of a refined estimate of GDP growth for the end of last year and the industrial PMI index - data that may influence the Czech National Bank's outlook for monetary policy.

The Prague Stock Exchange ended last week under pressure. The PX index weakened by almost a percent to 2512.98 points, with most of the main titles losing ground. Only shares of Erste Bank, tobacco company Philip Morris ČR and solar power plant builder Photon Energy rose. The Czech koruna is under pressure from the conflict in the Strait of Hormuz - it is trading around CZK 24.39/EUR against the euro, with analysts warning that the complete halt of traffic in the Strait is putting sustained pressure on energy prices.

The arms sector remains an exception to the otherwise cautious market sentiment. Armaments Group CZG (Colt CZ) reported sales of EUR 6.7 billion last year, with a year-on-year increase of 72 %, or 30 % when the acquisition of Kinetic Group is taken into account. Adjusted EBITDA rose to EUR1.63bn. The company has set its revenue guidance for this year in the range of CZK30bn-33bn and proposed a dividend of CZK30 per share. It also plans to continue its share buyback programme.

George mobile app by Czech Savings Banks has received a security boost. A new cybersecurity algorithm detects potentially fraudulent transactions, with a red warning screen appearing not only in mobile but also in online banking from February 2026. Česká spořitelna has also opened up space for the issuance of specific securities aimed at large institutional investors such as pension funds - a move that comes at a time of intense recovery in the domestic mortgage market.

The industrial sector follows the development in the metallurgical company Liberty Ostrava. Šimon Peták, the insolvency administrator, has terminated the collective agreement valid for employees until the end of 2026 and wants to update its terms because they do not correspond to the current economic and operational possibilities of the company. The notice period is six months. In the meantime, the court has approved the sale of the smelter to a consortium of companies owned by former Interior Minister Martin Pecina for CZK 3.01 billion, but the sale has not yet been approved by the Office for the Protection of Competition.

The government coalition is working on legislation to speed up the removal of tariffs on industrial goods from the United States - the European Commission is trying to push this legislation through as soon as possible.

Foreign investment

The global M&A market has been dominated in recent days by large transactions that also have a direct impact on the European energy and industrial sectors.

The most significant transaction of the end of March remains the takeover of a Canadian renewable energy producer Boralex. Brookfield Asset Management and La Caisse have signed an agreement to acquire Quebec energy company Boralex for CAD 37.25 per share, implying a total equity value of approximately CAD 3.8 billion. The transaction brings the total enterprise value to $9 billion. La Caisse will increase its stake from approximately 15 % to 30 %, while Brookfield, along with its institutional partners, including Brookfield Renewable Partners, will hold the remaining 70 %. The transaction, which is expected to close in the fourth quarter of 2026, strengthens both investors' position in the energy transition sector in North America and Europe.

In the technology and media sector, the previously announced acquisition is still in focus Warner Bros. Discovery by Netflix for approximately $82.7 billion, one of the largest media transactions ever. The turn of March and April also brings the continued integration of the Verizon-purchased Frontier Communications a $20 billion connection that will give the company a reach of nearly 30 million fiber-optic connections in 31 U.S. states.

Investment bank Goldman Sachs is rewriting its forecasts and according to its analysts, the ECB will raise interest rates twice this year - in April and June. JPMorgan and Barclays expect as many as three rate hikes in the eurozone due to the risk of higher inflation caused by geopolitical tensions. This would most likely imply the need for a response for the CNB as well.

Skoda Group meanwhile, confirmed talks with Indian Prime Minister Modi on a strategic expansion into the Indian market, which could open the way for more industrial contracts in the fast-growing Asian economy.

On the global M&A scene, the rapidly advancing integration in the field of artificial intelligence is attracting attention - technology giants Nvidia a SLB expand AI partnerships for energy infrastructure, while the company IonQ announced plans to acquire chipmaker SkyWater Technology for $1.8 billion to build its own quantum computing platforms.

Significant events outside the Czech Republic with global impact

The geopolitical situation around Iran remains a dominant theme for global energy markets. The conflict, which erupted with the US-Israeli attacks on Iran in late February 2026, has crippled shipping in the Strait of Hormuz, through which approximately one-fifth of the world's oil and gas supplies normally flow.

Oil prices rose by more than three percentage points on Thursday, March 27, with North Sea Brent crude exceeding $106 a barrel and US WTI trading around $93. U.S. President Donald Trump extended until April 6 the period when the U.S. will not attack Iran's energy infrastructure, but markets did not react to the move by falling prices. Tehran promptly denied the diplomatic contacts and geopolitical tensions rose further following the Yemeni Houthi attack on Israel.

On Thursday, the OECD cut its growth outlook for the euro area and forecast higher inflation for 2026 due to soaring energy prices. The conflict has also weighed on German consumer sentiment, which fell before the start of April.

Analysts at Goldman Sachs, Moody's Analytics and EY Parthenon are raising their estimates of the likelihood of a US recession. Moody's currently estimates it at nearly 49 %, Goldman Sachs at 30 % and EY Parthenon at up to 40 %. Economists agree that if oil prices remain at current levels until the end of the second quarter, a recession is likely.

The turn of March and April thus brings significant uncertainty to the global and Czech economy - the energy crisis caused by the Iranian conflict threatens price stability, but at the same time paradoxically strengthens the arms sector and accelerates the energy transition in Europe. In particular, the key factor for the second quarter will be whether traffic in the Strait of Hormuz can be resumed and whether diplomatic negotiations will yield results.

gnews.cz - GH

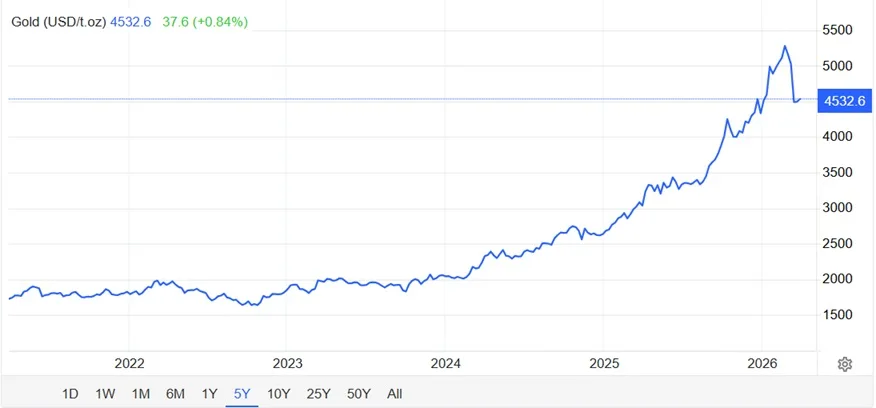

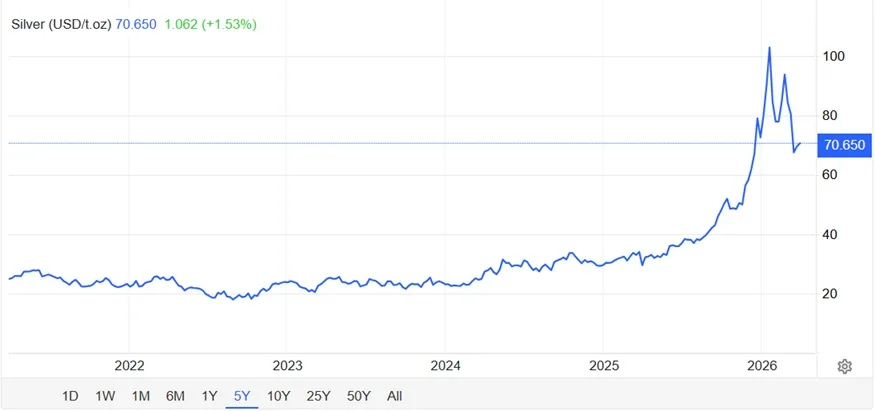

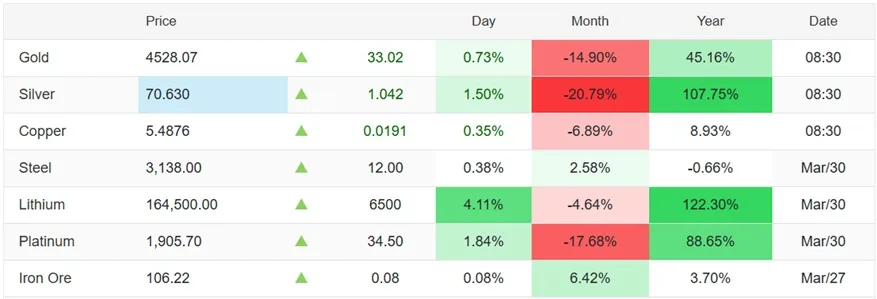

[currency_and_metal_rates]

tradingeconomics.com